Monthly Update #13 December 2019 – The Donation Milestone Is Over

Hi everybody,

First of all, happy new year, hope everyone had a nice Christmas time and a powerful 2020 start?

As it tends to be, the last month of 2019 was rather busy. All of the sudden, you need to decide what gifts to purchase for your loved ones (hard!), then you need to find them on the cheapest retail store (yes, I ended up buying them on Amazon anyway, LOL), then make sure no one is at home when the gifts arrive (I chose my workplace address to be safe), after that, then hide them in a place where won’t be found until you got some “only you time” to wrap them up and hide them back 🙂

If that sounds like exciting to you then you are a Christmas lover, if not Bah humbug! I personally enjoyed it in spit of the costing.

For the first time ever, I and my misses spent Christmas in my hometown. After spending the previous two in England, it was an odd feeling, as I also visited my mum regularly to her care home, Christmas Eve and day included.

Besides this, we spent a couple of days in Andorra, which looks awesome during the festive times, and enjoyed a session on the spa-resort Caldea (fully recommended) to celebrate GF’s birthday.

Andorra, due to its tax advantages, is an interesting city to explore, especially for the financial independence community. I did consider myself selling all my real estate assets at some point in the future and relocate there. However, I am more a guy of being close to the seawater, rather than high cold mountains and ski resorts, so the Canary Islands sounds a bit better to me, and it also has some tax advantages.

Anyway, if interested in Andorra, then I would recommend you to listen to this episode from the financial independence Europe podcast, which is full of useful information about the independent principality.

Table of Contents

Thoughts From The Current P2P Outlook

December was another eventful month for the peer-to-peer lending industry, although this time its main focus came from Europe instead of the UK.

If you are a P2P investor, then I am 100% convinced that you’ve read Explore P2P’s post about the questionable legality on the Alborg Petrol loan crowdfunded by Kuetzal platform, the concerns from the financially free blogger and the negative follow-up post after the meeting with the current Kuetzal CEO, Maksims Reutovs.

I am not a Kuetzal investor myself, so I am going to make this short.

As a peer-to-peer investor, I was expecting a scandal like that to happen sooner or later, and expect more to come. This one specifically didn’t affect me, but I know that at some point I’ll get my fingers trapped. From my personal point of view, the thing that can potentially protect me the most is “diversification”. Even if I spend hours and hours researching and think that I am enough well-informed to don’t diversify, I would still put diversification in front, and especially in the P2P lending market, where not all information is transparently revealed and many try to make a business from it.

Anyway, Kuetzal brings me a reminder about the risks of investing via peer-to-peer lending and how important it is to know and be aware of your own risk tolerance. If you are a P2P investor and panicked after the news, I would reconsider your asset allocation.

It’s also been useful to remind me that I still need to readapt my crowdlending portfolio distribution according to my unprofessional risk-reward assessment that I seem to keep postponing! 🙂

To the numbers.

Quick Recap of December Numbers

- Portfolio value: 108,764 € (+3%) – details HERE

- Monthly Transactions (Deposits – Withdrawals): 1,695 €

- Monthly growth from investments: 697 €

- Passive income: 593 € (+39 % ) – details HERE

- Savings rate: 55.8 %

Now, let’s get into the details.

Portfolio Performance

| Platform | Inception | Description | Value Nov. | Transactions | Growth | Value Dec. | Return Dec. | T. Return |

|---|---|---|---|---|---|---|---|---|

| Property Partner | 01/2018 | Buy-To-Let | 6,392 | -20 | 17 | 6,443 | 0.26 % | 5.16 % |

| Stocks & Shares ISA | 03/2018 | Stocks & Bonds | 56,356.2 | 920.4 | -6 | 58,242.4 | -0.01 % | 13.5 % |

| Housers | 03/2018 | BTL and Dev. Loans | 6,791 | 0 | 17 | 6,808 | 0.25 % | 6.1 % |

| Grupeer | 05/2018 | General P2P Lending | 8,687 | 0 | 106 | 8,793 | 1.2% | 25.3 % |

| Mintos | 08/2018 | General P2P Lending | 329 | - 47 | 4 | 285 | 1.1 % | 14.6 % |

| Crowdestate | 08/2018 | Development Loans | 2,104 | 185 | 19 | 2,308 | 0.92 % | 13.7 % |

| Envestio | 10/2018 | Business & Dev. Loans | 5,155 | -401 | 73 | 4,827 | 1.4 % | 23.1 % |

| Fast Invest | 10/2018 | Consumer Loans | 1,151.2 | 0 | 12.19 | 1,163.4 | 1.06 % | 16.3 % |

| Trading 212 | 03/2019 | Dividend Investing | 1,662.5 | 0 | 83.5 | 1,746 | 5.3 % | 61 % |

| Estateguru | 05/2019 | Development Loans | 3,116.3 | 0 | 33.5 | 3,149.8 | 1.08 % | 5,5 % |

| Abundance | 05/2019 | Business Loans (Ethycal) | 636.5 | 59 | 9.36 | 717 | 1.3 % | 3.6 % |

| RateSetter | 08/2019 | General P2P Lending | 1,186.11 | 0 | 2.97 | 1199.2 | 0.25 % | 1.63 % |

| Crowdestor | 08/2019 | Business & Dev. Loans | 2326.4 | 200 | 17.9 | 2,544 | 0.77 % | 4.21 % |

| Robocash | 08/2019 | General P2P Lending | 4050.6 | 0 | 39.4 | 4090 | 0.97 % | 3.6 % |

| Wisefund | 09/2019 | Business Loans | 2130.1 | -32 | 32.94 | 2131.1 | 1.55 % | 6.45 % |

| Freetrade | 09/2019 | REITs | 176.5 | 17.5 | 4.9 | 173.3 | 3 % | 8.9 % |

| Evoestate | 10/2019 | Buy-To-Let | 615 | 500 | 3.31 | 3.15 | 0.5 % | 4.1 % |

| UK Pension | 10/2019 | 100% Global Equity Fund | 2375** | 388.8 | 226.1 | 2,824** | 7.5 % | 39.3 % |

| TOTAL | 105,799 € | 1,695 € | 697 € | 108,764 € | +0.66 % | -36.2 % * |

*Includes Algotechs loss

**20 % discounted as future tax payments

In December I didn’t buy my third dividend stock, as I had planned last month. I spent a few hours researching but I gave up as couldn’t find anything convincing. I am not in a hurry to increase my dividend portfolio, so I may possibly wait for the next market dip and see if I can catch something cheaper. I did get, though, my “first” dividend payment of 3.7 Euros from Johnson & Johnson (JNJ) 🙂

Now back to the table, we can see that once again my best performer is my UK pension +7.5% followed by my Trading 212 dividend portfolio +5.3%.

The alternative side of my portfolio stays quite behind, my Free Trade REITs portfolio increased +3%, followed by Wisefund +1.55% and Envestio +1.4%.

The GBP/EUR currency ratio grows from 1.17 to 1.18, boosting the value of my Euro portfolio.

Stocks & Shares ISA

My stocks & shares ISA portfolio value shrinks £-5. The market losses £-154, bonds and cash interest is £80.34 and stock dividend £86.79. I was surprisingly paid twice, so I am assuming there won’t be any income in January.

As usual, I paid myself £780 out of my payslip as an automatic regular monthly payment.

As it was year-end, I rebalanced my stock-bond portfolio distribution back to a 50/50 proportion, as stocks had been going through the roof lately.

My best ETF performer is the S&P 500 UCITS (VUSA) +21.57%.

The worst performer so far is USD Treasury Bond UCITS ETF (VUTY) +0.95%

2019 returns:

- S&P 500 Index : +29%

- My balanced Vanguard ISA: +11.2 %

This year my ISA wasn’t as fortunate as the previous one, where it beat the market. I am totally fine with it, as I know these returns are good enough to keep up with my one million plan statement.

See further details and the portfolio chart in my Vanguard page

Property Partner

Rental Income from Property Partner is £18.68 (£18.68 in Nov). Steady. As a UK resident, this income is tax-free.

Everything is rather quiet here. Management went silent since the last increase in fees update and I have no changes in my portfolio this month.

Boris Johnson announced that minimum wages will increase by +6.2% in the UK, which is 3 times inflation. I am curious to see if that will affect positively the property prices of my portfolio.

See further details and the portfolio chart on Property Partner page

Related content: Property Partner Review & Property Partner Stabs Their Small Investors

Housers

Income from Housers in November was 17 EUR (15 EUR last month) This is income after-tax as it is automatically deducted from the platform.

Is still early days, but in 2020 I would like to cut down my Housers portfolio and invest through Evoestate instead.

See further details and the portfolio chart on Housers page.

Related content: Housers Review

Estateguru

Estateguru income is 33.5 EUR (34.6 EUR last month). My portfolio consists of 60 loans (59 last month), where 6 are delayed on payments (4 last month). 1 loan is delayed between 4-15 days, 3 loans are delayed between 16-30 days, and finally 2 loans between 31-60 days. None of my loans has defaulted.

I am happy with this platform so far. I like its transparency, profitability, low defaults ratio and success at recovering investors money from defaults. However, the XIRR after 8 months of investing stays behind the initially expected return. Let’s see how that develops after one year.

See further details and the portfolio chart on Estateguru page.

Crowdestate

My Crowdestate portfolio earns 19 EUR (11 EUR last month).

I received bad news in December from Crowdestate. It’s nothing wrong with the platform or company itself though.

From now on Crowdestate will start withholding taxes to me on all income from Italian investments to comply with the Italian law. We are talking about a 26% tax deductions. It also seems that income from Romanian projects is also affected.

I started “operation sell-off” on all my Italian investments. I am keeping the Romanian ones for now as the returns are higher.

My Crowdestate portfolio consists of 13 loans (13 last month), where only one is delayed.

See further details and the portfolio chart on Crowdestate page

Evoestate

The first rental income kicked in this month. Both of my buy-to-let properties from Brickstarter paid a total sum of 3.31 EUR.

I invested 500 EUR in the latest skin in the game BTF addition. This time an office building from Reinvest24*.

This is a screenshot of my current portfolio diversification.

See further details and the portfolio chart on Evoestate page

Grupeer

Grupeer has performed solidly, manufacturing another welcoming 106 EUR (94 EUR previous month) of passive income in December.

Returns this month are better than usual due to Grupeer’s December cashback campaigns. They also introduced some new loans with 14% interest rate, just like old times! YAY! 🙂

I love this platform but I will at some point reduce portfolio size to improve diversification.

See further details and the portfolio chart on Grupeer page

Related content: Grupeer review after 15 months of investing.

Envestio

Income from Envestio decreases down to 73 EUR (75 EUR last month).

Envestio was a bit late to issue new opportunities, so my impatience made me withdraw free cash from exited projects. In this respect, I rather Crowdestor, as it informs investors about future upcoming projects in advance, making it easier to make decisions on how to manage one’s own money.

However, recent management changes put me off slightly and I rather wait to see how the platform is operated from now forwards.

See further details and the portfolio chart on Envestio page

Fast Invest

Another solid month for Fast Invest returning 12.19 EUR (12.08 EUR previous month).

My auto-invest is set to invest in 13% loans or higher and it’s working fine, no cash drag issues.

Check out my returns after 14 months of investing and portfolio chart on Fast Invest page

Robocash

December is my fifth Robo-month 😉 returning 39.4 EUR (13.47 EUR last month). Excellent!

My auto-invest strategy is set to invest between 1-1300 EUR loans in a 1-367 days maturity with 12-13% return. With this configuration my cash drag is minimal.

The platform’s high profitability and its buyback guarantee make me feel rather safe to invest my money with them.

Current loans: 3,229.57 EUR

Overdue loans: 860.43 EUR

See further details and the portfolio chart on Robocash Page

RateSetter

RateSetter paid an interest of £2.97 (£13.77 last month)

I allocated all my funds in a Max Account which initially gave a 5% interest. This is pretty low when compared with other P2P lending platforms, but at least the returns are tax-free as long as I reside in the UK and I don’t surpass the £1000 annual interest allowance from FCA regulated financial services (which doesn’t include EU platforms)

Furthermore, I should receive a £100 bonus after a year of investing with RateSetter that should propel my returns up to 15%.

See further details and the portfolio chart on RateSetter page

Crowdestor

Crowdestor returned 17.9 EUR (35.88 EUR last month).

The longer I invest with Crowdestor, the more I like it. The transparency levels are greater than in Envestio, as well as its investment opportunities flow. The coming soon projects section is ideal to get a plan ahead of your next investment moves.

In addition to all of this, Crowdestor did something quite special during Christmas. It crowdfunded 5,608€ as a charity project for a Latvian Orphanage Fund to support children in need and also orphans.

I absolutely loved it and convinced me to donate my first 100 EUR! 🙂

Ok, I´ve just made my first donation of 100€ out of my 2019 blog income to @crowdestor´s crowdfunding donation for supporting children with special needs and orphans.

— Tony @ OneMillionJourney.com (@JourneyMillion) December 20, 2019

Find out more ? https://t.co/AUPBMaXDk0

Thanks to those who trusted me and used some of my affiliate links. pic.twitter.com/5uASpUaZrx

See further details and the portfolio chart on Crowdestor page.

Wisefund

Wisefund returns 32.94 EUR (32 EUR last month)

The technical improvement update on automated deposit processing took over a month, which is much longer than what they initially told us. As a start-up, I take this as a lack of experience in the business, but it has lowered my confidence and I don’t plan to add more funds in for the time being.

See further details and the portfolio chart on Wisefund page

The €45K Project Fund

As usual, my savings on tobacco as a non-smoker went straight away to my Abundance account. That’s another £50 that I invested in the latest ethical investment.

For this tax year, the whole €45K Project Fund is invested in Abundance, as I am using an IF ISA account (tax-free).

So far, I have recovered the 1.59% of my loss = 717 EUR

44,283 EUR left to go.

See further details and the portfolio chart in the Abundance page

Related content: How I FIRED 45k with algo trading, Investing Ethically, Recovering €45K through Investing in Myself First

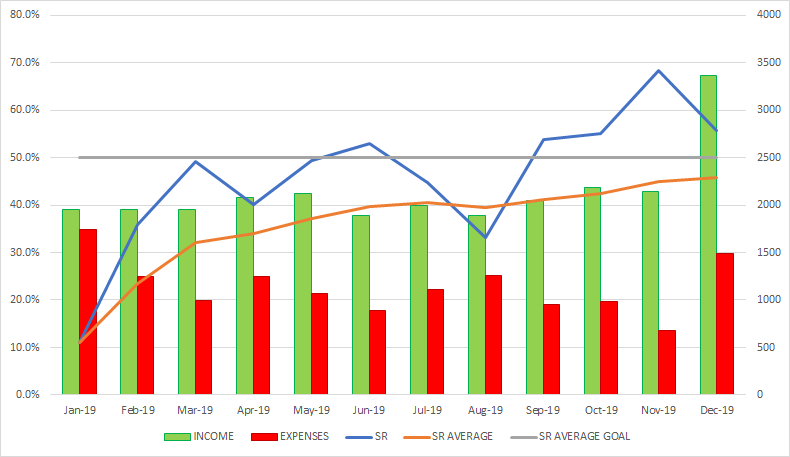

Savings Rate

My total net income in December was £3.359.7 (3,964.4 EUR) and my expenses were £1,486.9.

I was able to save £1872.8 in December. That results in a savings rate of 55.7%

This is pretty good as December is a much more expensive month 😀

My expenses were higher but so was my net income, as I received a bonus from work and a cash gift from mum. Lucky me!

I added my monthly income and expenses on the chart.

Income, expenses and savings during 2019

In 2019 I received a total net income of £25,579 or 30,183 EUR (passive income not included)

I spent a total of £13,657 or 16,115 EUR and saved £11,922.5 or 14,068 EUR

My average monthly expenses reference I had for my FI ratio calculations was 1200 EUR. In 2019 I spent more than I thought I would and the average increases to 1300 EUR a month. The increase in the Pound value has also affected.

My savings ratio for 2019 is 46%.

One of my goals for 2020 is to increase this to at least 50%.

Health

I kept a healthy running routine during the first two and a half weeks of December. Then during my Christmas time in Spain, my jaw was the head runner!

My resting heart rate still stays at 63 bpm, as the previous month. The issue is now my weight and body fat, which is worrying. I am the fattest since I can remember, and I don’t feel too good about it.

BUT, I am going to get this changed in 2020!

The donation milestone is over

Some more people used my links this month, thank you for doing so.

My total income since January from Targetcicle is 268.05 EUR (169.61 EUR last month)

Besides this income, I’ve got £3 from Property Partner, 75 EUR from Housers, 60 EUR from Evoestate and 8 EUR from Trading 212.

That makes a total blog income of approximately 415 EUR in 2019, which is almost halfway to my 1000 EUR donation goal. Great! 🙂

As I promised, I am going to donate this money. So far I’ve only donated 100 EUR to Crowdestor’s charity project.

I will donate the resting 315 EUR to Gates and Melinda foundation. The local charity didn’t work out and I don’t trust them much. The minimum donation amount was the sponsorship of £450 a year, to pay for the full year education of a child in Kenia. The idea of posting a picture of a sponsored child on the blog was exciting, but they didn’t agree to break down the budget for me and it also quite ties you to donate year after year the amount that is set to renew sponsorship, as stopping child’s studying career would be hard.

So,

Bill’s won it after watching the Inside Bill’s Brain documentary from my girlfriend’s Netflix membership. Hopefully, I should be able to post a donation proof on my next monthly update.

As I am still far from my donation goal, in 2020 I will donate 50% of my blog income. However, I don’t think I will display it as transparently as I have so far, or even if I will share my blog income at all.

Once again, thanks to those who intentionally used my links last year.

Joining links and offers

Property Partner (share up to £1500, details here)

Estate Guru (0.5% bonus on your investments made during the first 3 months)

Mintos (0.5% bonus on your investments made during the first 3 months – UK residents temporally not accepted)

Housers (25 EUR cashback for a minimum investment of 50 EUR)

Evoestate (15 EUR cashback for a minimum investment of 50 EUR)

Grupeer

Fast Invest

Crowdestate

Crowdestor

Trading 212 Trading platform UK and EU (Free shares worth up to $/£/EUR 100 )

Freetrade Trading platform UK (Free share worth up £200)

Thanks for reading! 😀

Have a great January all 😀

You can follow me on Twitter where I share some thoughts from time to time and connect with other like-minded people. You can also follow me on Facebook.

Disclaimer: Most of the links on this post are affiliate or referral ones. If you join to a platform using my affiliate links you may get a bonus or commission and so could I. I’m going to donate 50% of any commission I get throughout 2020 to a charity. You can read more about the purposes of this blog here and where this money is going to go here. Thanks.

Share this:

12 Comments

Comments are closed.

ABOUT ME

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

NET WORTH GOAL

Have you considered investing in tfg crowd?

Hi Marcus,

Yes I have considered adding TFGcrowd as a business loan platform, but I am focusing on rebalancing my portfolio before entering any new one.

Are you a TFGcrowd user yourself? If so, are you happy so far with the platform?

I see that you are trying to cut down your piece in Housers. I tried to do the same but have quite some issues with selling. Some of the parts of properties I own are not selling at all, even with quite a good discount. So make sure to expect that to take some time and/or money!

Hi Lazyinvestor,

Yup, the liquidity on Housers is near zero lately. There’s way too much marketing and cash offers for investors to fund new investments that the secondary market has become forgotten. However, my plan is to reduce my portfolio step by step, simply by not reinvesting interest income or principal from exited opportunities. When I first invested in Housers I was fully aware that my money could be tied up on the platform for over 5 years. So I am fine with it.

Happy New Year Tony!

I, like you, am just waiting for the market to come down a little bit before I purchase any stocks.

Currently I have a little list of stocks that have increased their dividends each year over the last 15+ years.

For me, I think that is where some real value comes from. The pullback will definitely happen, it’s just a matter of when!

You have hit your savings rate for the last 4 months now. Time to increase the goal?

Look forward to your updates throughout 2020.

Matt / thewahman

Hey Matt glad to see I am not the only one waiting 🙂

As you say, is a matter of when though. Statistically, the market corrects once per year, will see. This year is odd as there is the US election on the way.

That’s not a bad idea, maybe once I get to the 50% average I ‘ll think about increasing it 🙂

Thanks, me too Matt.

Hey Tony, just curious what brought this on: However, I don’t think I will display it as transparently as I have so far, or even if I will share my blog income at all.

? 🙂

Hey Nick, I am still unclear on what I will end up doing, but there are several reasons that are making me ponder.

1 – It seems that people generally associate blog income with success, this being the main interest for many visitors – it’s not a good feeling.

2 – Tradingcicle wasn’t extremely happy at first when I asked if I could share a dashboard screenshot of my income, they agreed as per donation purposes and with restrictions. Now in 2020, I won’t donate the full amount (maybe they don’t care anymore, I haven’t reconfirmed this year)

3 – I would still share all my blog income at the year-end, before donating half. I don’t donate as I receive like you. I invest as I receive and donate once a year.

As said though I am still thinking about it, as on the other hand, it doesn’t seem right to hide number on a FI blog.

I am trying to digest your 2020 goal, you started the year strong! 🙂

Raising nearly £500 for charity over the last year is a great effort. Well done! And considering that most of that income probably came in the latter half of the year, I imagine and hope that you will be able to earn and therefore donate even more in 2020.

My RateSetter bonus recently came through, taking my effective interest rate to around 14% from them for the year. I’ve since emptied the account though, as I will soon need that money for wedding and visa costs!

Good to read that you had a good Christmas, and all the best for the upcoming year!

Thanks Doc. for your nice comment. I am quite happy with the money I was able to raise in the end. You are right, most of it came over the last 6 months as during the first ones I was barely raising 5 or 10 as much.

We’ll see what 2020 brings 🙂 Glad to see it came through, I still got a few more months to go before I get the bonus from Ratesetter.

All the best for 2020 amigo 🙂

[…] having a messy P2P portfolio caused by promotions, bonuses, or cashback deals. As I mentioned in my December’s update, the latest problematic issue with Kuetzal recalled me that I still got some homework to do to […]

[…] October was an excellent passive income month for me. I earned 446.9 € which could have covered 40.5% of my monthly expenses. The last time I crossed the 4 hundred line of passive income was back in December 2019. […]