Peer to Peer Lending Risks To Be Aware Of

This post contains a collected summary of the several peer to peer lending risks that need to be considered by any investor who wishes to use this investment vehicle as a wealth grower tool.

The onemillionjourney blog has been getting more attention from the P2P community after the last feature as a top 50 P2P lending blog to follow in 2019 from learnbonds.

Hence, as more people are landing on my site in regards to find information on that topic, I thought it would be a good idea to create a post where I collect and lay down the investments risks derived from investing in the peer-to-peer lending platforms.

Normally, everyone can find the main risks well displayed on the platform’s website. These should be explained most of the times on a page or blog post. We may also find more information on the FAQ (Frequently asked questions) section, so don’t forget to always check this out.

Table of Contents

Peer to peer lending risks

The peer-to-peer lending, or also called P2P, has been gaining traction over the last decade, especially during the last 5 years, where the fintech industry has seen a boom of P2P platforms offering several types of investment to users. The mono-banking culture we have had since the 1990 seems to be on its way out, removing the middleman and adding an efficient form of alternative finance.

Some people are fascinated by how the fintech industry is changing the rules of the game. That probably includes millennials, software developers (the creators) or engineers (myself).

The biggest and major risk though, from my point of view, is that there is no need to have any financial background to invest in this market. The entry barriers are low, investors need small amounts of cash and there are no license or special requirements needed.

Good news is that if you are reading this post then you are already mitigating the biggest risk; oneself, by adding related information into your brains.

In this article you’ll also find other valuable resources I found interesting and worth a read.

Let’s review the peer to peer lending risks that everyone should know about peer-to-peer-lending, regardless you are a newbie or a veteran investor.

Borrower defaults

Some P2P lending platforms will argue that their team does an in deep due diligence on their loan originators or individual borrowers. While it may sound very convincing at first, we must remember that some borrowers are likely to default sooner or later, therefore losing a percentage of our principal investments CAN happen.

The image down below shows the loans risk classes and their historical default rate consisting of 70,673 loan observations from the Lending Club, the first Peer-to-Peer lender registered in the US, 13 years ago.

You can read the full research on the MDPI site.

As we can see, even the Low-Risk Class (Loan A grade) carries a historical default rate of 6.6%, so that’s something to bear in mind in your expectations.

How to minimise the risks?

In Europe, some P2P platforms have opted to introduce the buyback guarantees model to lower the defaulting risks. It is a guarantee provided by a loan originator regarding a specific loan. If repayment of that loan is delayed by more than a specified number of days (usually 60 or 90), then the loan originator is obligated to buy back the loan.

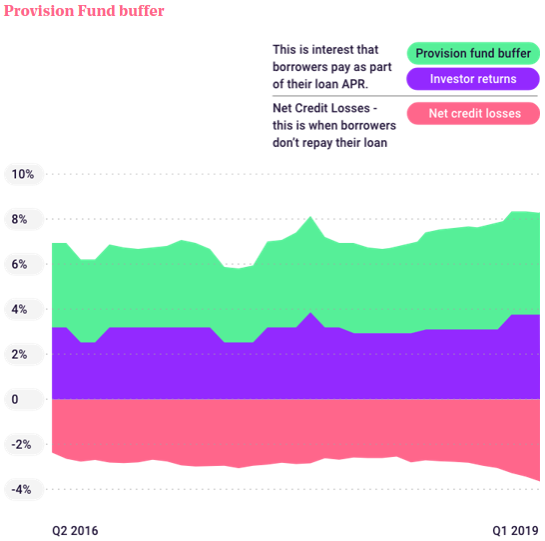

Other platforms keep a provision fund, which will be used to buy any defaulted loans and return the capital back to investors. These provision funds vary widely from one site to another, so make sure you know what’s covered if you’re thinking of becoming a lender.

For instance, RateSetter’s* provision fund grows along with the portfolio size and repayments made by borrowers. The money that is in the provision fund is a buffer to protect investments. It does this by automatically reimbursing if a borrower’s payment is missed.

* Referral link. If you join using this link you will be given £100 cash back if investing £1000 for a year.

This adds an extra layer of safety, but some argue that it’s being overused as a marketing strategy to attract more investors and that it would be worthless to mitigate others risks in a case of an economic meltdown.

Some of these other risks could be…

Loan originator defaults

As I briefly explained in my quick to read post “Investing for beginners – how to get started” Some P2P platforms are only the middlemen between borrowers and loan originators and do not deal with borrowers directly.

This adds the possibility of a loan originator defaulting as a risk to be considered.

For instance, one of your investment may be protected by a buyback guarantee from the loan originator, but if it becomes insolvent then there is no one to bring you back your money.

That happening doesn’t mean that you’ve lost your money completely, but you will lose liquidity, having no access to your cash for a certain period.

Normally all investors who have been affected by a failing loan originator are represented as a group by lawyers appointed by the platform for this matter.

So, be aware that you should invest only money that you can afford to lose and won’t need any time soon, same as with any other investment.

How to minimise the risks?

That depends on the amount of time that you are willing to spend.

If you have plenty of time, enjoy researching, reading financial statement and reviews, then spending time on doing a deep due diligence on every loan originator may be the way. Choose those that look attractive, financially healthy and safer to you.

But, most of the people don’t have the luxury of having a lot of free time or would rather spend it doing other things. Then there’s only one answer:

Diversifying as much as possible across different loan originators is the key, the more the better.

P2P lending site going bust

This is the most feared risk as it could potentially involve losing a big chunk of your money if not all.

If the platform we deal with is not regulated, there may be a chance that you become a victim of fraud.

For instance, take the example of China, whose P2P lending market boomed from one platform in 2007 to over 3,448 platforms in 2015. Unfortunately, nothing expands forever and by the end of 2015, there were 1,031 total troubled platforms, that’s one out of four having problems approximately.

Source: Techcrunch

In 2016, statistics released by the Chinese Banking Regulatory Commission showed that about 40% of P2P lending platforms were, in fact, Ponzi schemes.

Source: Finextra

If the P2P lending market in China intrigues you, then you’ll find the following article interesting:

The Future of P2P Lending in China: Is There a Time After the Great Cleanup?

The chances of dealing with a Ponzi Scheme in the UK are lower as they all must be regulated by the Financial Conduct Authority (FCA), which states that platforms must allocate investors’ money in segregated accounts. That means If the company bankrupts it has no access to investors’ money, mitigating the risk of fraud.

The UK FCA has also mandated that P2P lending companies must appoint a Trustee to continue serve lenders and borrowers, controlling payments as per schedule and keeping investors’ money away from the company. So, in case the company is gone there will be someone else to manage it all for you.

Unfortunately, in

No clear regulation means that every single platform can follow a different system (= extra time required on research).

How to minimise risks?

It is extremely important to read as much as possible about the platform you are interested to invest in before going ahead. Find out how the platform protects investors’ money as every platform may work differently.

Needless to say, diversifying across several platforms helps again to lower the risks. If I had the choice to start over from scratch again, I would first invest in platforms that have built trust around the P2P community by deploying low amounts to see whether I feel comfortable with this type of alternative investing before going big. Then, once I see I can deal with it, I would likely increase my P2P portfolio, diversifying among several P2P lending companies that have, again, shown trustworthiness.

Cash Drag

Your money may not be lent straight away, meaning that you won’t get any return on cash sitting on the platform. That can happen after your first deposit or after your interest or principal payments. If the loan book on the platform is not big enough to meet investors moneys demands then some of your cash won’t be working for you, that’s called cash drag.

How to minimise risks?

Cash drag is not a big issue, but it is important to consider as it can lower your calculated returns in your investing plan.

Most platforms use what’s called the auto-invest feature. This will allow the software to reinvest your money automatically for you, ensuring that funds are invested all the time, helping you on maximising returns.

However, loan availability and investors capital isn’t constant, and to keep these two variables in a harmonic shape isn’t always possible, although top platforms like Mintos or Grupeer are doing a great job so far.

Psychological risks

This risk is present in every investment, and that’s yourself. Carelessness, greed, panic, pride and fear can all get the better of us sometimes!

As I mentioned briefly in the introduction, for some people this is the higher risks of all. If you are emotionally driven easily and change your opinion or investing principles often, then P2P lending may not be your call.

From my own experience, P2P lending platforms can be lucrative, extremely lucrative actually! Cash back offers, bonuses, referral programs and tempting high returns offering a new stream of income effortlessly. Everyone’s at it, and FOMO (feeling of missing out) starts digging in our minds.

This can make some people overlook the risks and allocate high percentages of their

The FCA has noticed this investing behaviour among P2P investors and has introduced a new rule where it is placing a limit on investments in P2P agreements for retail customers new to the sector of 10 per cent of investable assets.

For European platform there is no limit, yet.

This type of investing is relatively new, and though we have some historical data on how a quality P2P lender may perform during a recession (Zopa returned 4% during 2008-2009), it isn’t enough to confirm a positive general outlook for this market during the next economic downturn.

Technology Risks

The creative minds behind the latest trends in technology and software engineering firms are the initial creators of P2P lending market as an industry itself (Fintech). Therefore, given the fact that the platforms are based online, a cyber security breach is a possibility as they can be attractive targets for hackers.

How to minimize the risks

Some platforms as Fast Invest, Crowdestate or Robocash give you the chance to set up a two steps verification to log in. Also, don’t forget to protect your computer with effective software and to change your password periodically.

Market risks

Another set of risks to be aware of are those related to the market, which is in fact related to economic factors, such as changes in interest rates, a rise on unemployment rates, decrease on consumer spending and the devaluation of real estate or assets used as collateral protection for our investments. This plays an important role within the peer to peer lending risks.

For instance, you may be in a long-term loan that pays you 5% interest for an agreed term of 5 years. If national banks were to raise interest rates above your current return, then you will be “underperforming” the current scenario. That involves a risk, as if that would happen to you, you would rather have your funds in your savings account rather than in a P2P lender in terms of risk-reward. However, EU platforms offer, as an average, around 12% at the time of writing, whereas the US Treasury bonds yields 2.5%. The FED would have to raise interests by 9.5 points before levelling up with the majority of EU P2P lender, that’s quite a large “margin of safety”. In addition, when considering the current market scenario that’s unlikely to happen. (rates decrease when markets crashes).

Finally, the latest risk I’d like to highlight is the currency risk. Albeit the Euro is the main currency in EU, there are countries like Czech Republic that still use their own one and hence “suffer” from a currency risk when investing in European loans. In addition, some P2P platforms deal with loan originators from across the world (e.g. Russia or Mexico) that operate with non-Euro currencies. Volatility on the currency exchange (e.g. Pound/Euro after UK Referendum in 2016) may put some loan originators under some stress.

Final words

If you’ve reached the end of the post, then you may be scared about all the peer to peer lending risks. The truth is that every investment carries a certain level of risk. This type of alternative investing is generally categorised as a

Everyone is the master of their fate, and the captain of their soul

Napoleon Hill

An obviously that also makes you the captain of your investments. Once you are on board, you can neither control nor prevent the weather conditions you will encounter while you captain your ship, but you can master the fate of your investments by being aware of thei risks and diversifying wisely.

In terms of maximum allocation, I would take the 10% of your investable assets recommended by the UK FCA as rule of thumb, but remember I am not a qualified advisor. Please read my disclaimer at the bottom.

Seek real professional advice if unsure.

Finally, take my portfolio as an example of what could happen when someone doesn’t know what is doing and don’t diversify his investments.

Hope this article was useful to you.

Is there any other risk I am missing out?

Please, let me know down below the comments.

Other references:

Moneyadviceservice – Peer-to-Peer lending what you need to know

4thway – The Five Key Risks In Peer-To-Peer Lending

Orcamoney – P2P Lending Risks

RadicalFire – Peer-to-Peer Lending safety

Share this:

17 Comments

Comments are closed.

ABOUT ME

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

NET WORTH GOAL

Thank you for this!

My biggest fear in P2P is an economic downturn / recession. But I believe that the next crash is not like in 2008 so P2P-platforms will do ok.

– FN

Its hard to say how the next recession will be like. Historically, there hasn’t been 2 consecutive crashes triggered by the same factors. So, yeah I would hopefully expect not having another global financial crisis like in 2008, but…

Great article, Tony! I think you are right to highlight the FCA’s rule of thumb that you shouldn’t invest more than 10% of your income in P2P. It’s offered good returns up until now, but we don’t know how it will fare in a recession!

[…] note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]

[…] note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]

[…] note, links containing an asterisk (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]

[…] note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]

[…] note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]

[…] note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]

[…] note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]

[…] note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]

[…] The risk-rewards analysis is based upon the peer-to-peer lending risks I summarised on this post. […]

[…] note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]

[…] aren’t getting into the right shape. I interacted with some peeps on Twitter after posting my peer-to-peer lending risk posts, who confirmed liquidity issues and long waiting times to access their funds with the […]

[…] note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]

[…] note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]

[…] note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these […]